Market downturns can be unsettling. Investors observe their portfolio values decrease while they question their next financial steps. Market downturns create a special chance for investors to take financial action despite initial feelings of inaction. Strategies exist to position investments for long-term benefits during market dips. Tax-advantaged retirement accounts represent one of these investment strategies.

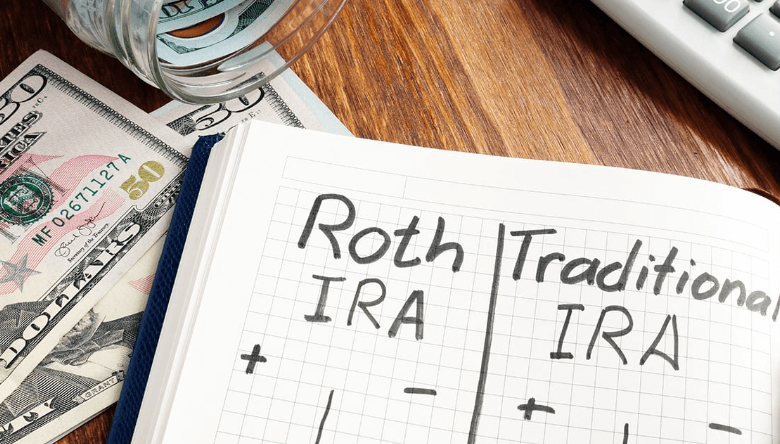

Lower Asset Values Mean Lower Taxes

The decrease in market value leads to lower investment worth. The short-term frustration of lower asset values transforms into a beneficial situation for investors. Investors who transfer their traditional retirement funds into Roth IRAs during market declines must pay taxes on the reduced account value. The tax basis used for taxation depends on the conversion value, so lower asset values lead to reduced tax obligations.

The market eventually rebounds. Investments recover their value when market conditions improve. The gains within Roth IRA accounts remain tax-free. Investors obtain a reduced tax burden by paying their taxes in advance rather than deferring payment until later. The impact on total retirement savings becomes substantial through this approach.

See also: The Future of Paralegal Services: Embracing Technology and Specialization

The Advantage of a Future Tax-Free Growth

One of the biggest benefits of a Roth IRA is tax-free withdrawals in retirement. Traditional retirement accounts require paying taxes on withdrawals, which can be unpredictable. Tax rates change over time, and future income levels may push investors into a higher bracket.

By shifting funds to a Roth IRA, taxes are locked in at today’s rates.

This removes uncertainty. Future withdrawals will not be affected by tax changes, creating a more stable retirement income. The peace of mind that comes with knowing retirement funds are not subject to future tax hikes is invaluable.

Market Timing and Smart Investing

Timing the market is difficult, but downturns create windows of opportunity. Investors who convert funds when prices are lower set themselves up for greater growth. The key is patience. When assets recover in a Roth IRA, those gains are protected from taxation.

Some investors hesitate, fearing further declines. While waiting for the absolute bottom is tempting, it is nearly impossible to predict. Gradual conversions over time can smooth out market fluctuations. This approach reduces the risk of making a move at the wrong moment.

Why a Roth Conversion Fits Different Investment Goals?

A Roth IRA works well for those expecting higher tax rates in retirement. It also benefits those who want to leave tax-free assets to heirs. Unlike traditional accounts, a Roth IRA has no required minimum distributions. This means funds can stay invested longer, growing without forced withdrawals.

For younger investors, a conversion during a downturn means decades of tax-free growth. For retirees, it provides flexibility. It allows better control over taxable income, helping to avoid higher Medicare premiums or Social Security taxes.

Managing the Tax Bill Strategically

The biggest hurdle with converting funds is the immediate tax cost. The amount moved into a Roth IRA is considered taxable income. If too much is converted in one year, it can push an investor into a higher tax bracket.

Spreading conversions over multiple years can minimize this impact. By staying within a lower tax bracket each year, investors reduce their total tax burden. Some also use deductions, credits, or previous losses to offset the tax bill.

Choosing the Right Time to Convert

No one can predict market movements with certainty, but certain signs suggest a good time to act. When stock prices fall significantly, a Roth IRA conversion becomes more attractive. A weaker economy, rising interest rates, or global uncertainty often push markets lower. These moments create prime opportunities for tax-efficient moves.

Personal financial situations also matter. Those with lower income in a given year may find it easier to handle the tax burden. Retirees before Social Security benefits begin or workers between jobs may find lower-income years ideal for conversions.

Conclusion

While a market downturn may feel discouraging, it offers unique advantages. Lower asset values reduce the tax cost of converting retirement savings. A Roth IRA provides long-term benefits, shielding future withdrawals from taxes. This creates financial security and flexibility. Making the right move requires careful planning. Consulting with a financial professional can help navigate the tax implications. With patience and strategy, investors can turn market uncertainty into an advantage. Thinking long-term often leads to the best outcomes, even during uncertain times.